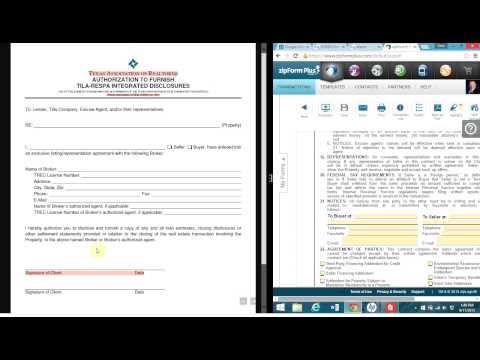

Max four corners with a couple of important updates starting on October second. - There is a new form that RESPA is going to require you to have to received any information from either the title company or the lender regarding transactions that you're going to be dealing with. - This is either with the seller or the buyer. - This is the first thing that you need to be aware of. - This is a new form that Tiller RESPA integrated disclosures. - You'll have to have it signed by you, the seller, and the buyer. - Your information and signature need to be included. - The reason you need this disclosure is because it states, "I hereby authorize you to disclose and furnish a copy of any and all loan estimates, closing disclosures, or other settlements statements provided in relation to the real estate transaction involving the property." - If your client wants you to take a look at the HUD statement to make sure everything is correct, the title company can no longer send this over to you without having this form signed by you. - Therefore, it is very important that you have this form in your packet from now on. - Another important point is that in the contract, paragraph 21, if you do not have your information filled out here, you will not receive a copy of anything from the title company. - The title company is not going to be authorized or allowed to send you anything in regards to any of the HLA disclosures or anything else relating to the contract. - Both of these things will need to be filled out with your information for you to get anything. - If you have any questions, please let me know. - Chris Harden, Remax four corners. - Email: CH AR d en at...

Award-winning PDF software

Respa exemptions Form: What You Should Know

A. Ask for a builder ID. B. The builder has to provide ID that is linked to the loan application (e.g. Social Security number, Builder ID number). C. This ID is required when an item is built.

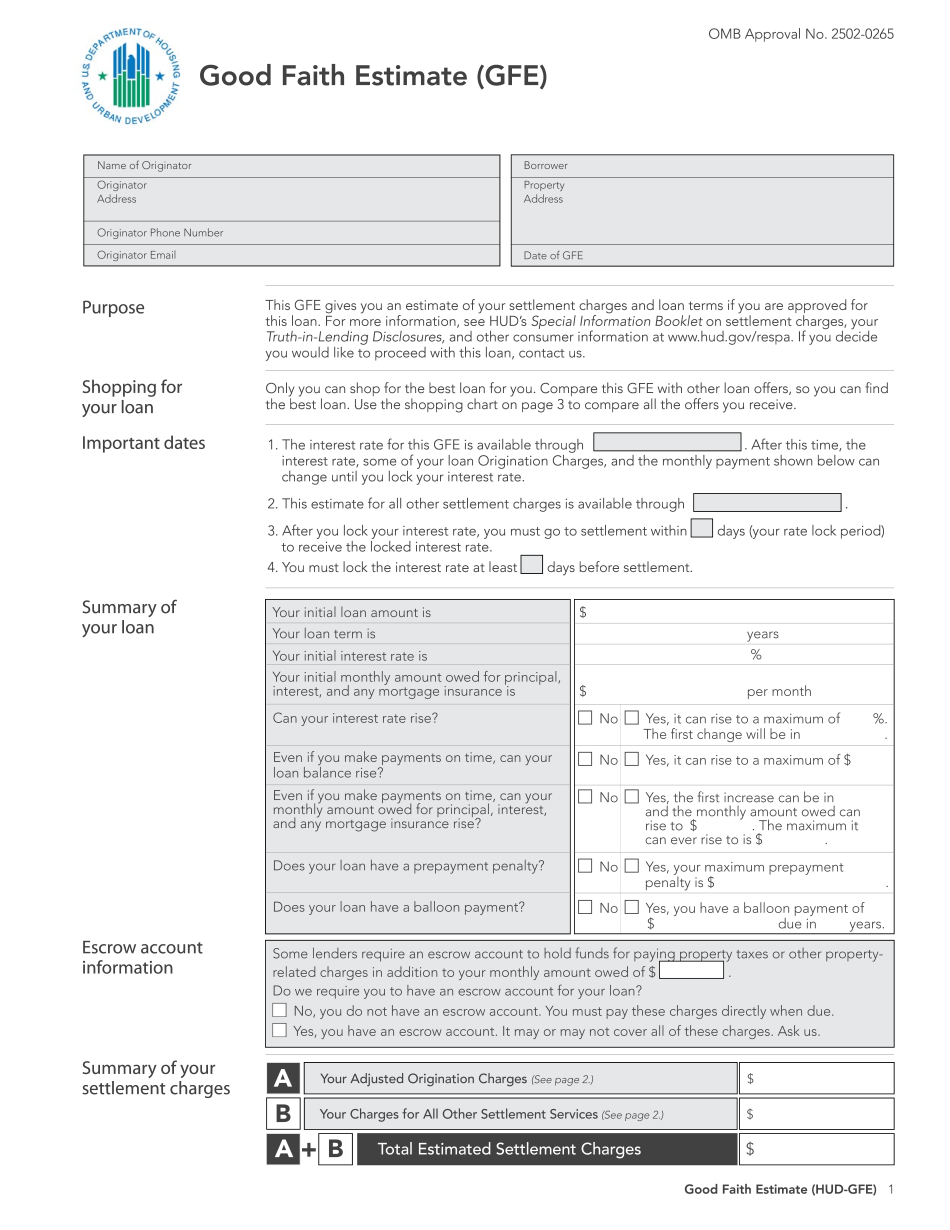

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do HUD-Gfe, steer clear of blunders along with furnish it in a timely manner:

How to complete any HUD-Gfe Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your HUD-Gfe by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your HUD-Gfe from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Respa exemptions