1. So, Atilla regulations in Philadelphia credit a PR and advertising. 2. Atilla deals with credit, a PR, and advertising of consumer lives. 3. It requires lenders to disclose the complete cost of credit. 4. What do I mean when I say requires them to disclose the complete cost of credit? 5. Pistol audison, they have to tell you the whole story upfront. 6. For example, yes you're buying this house for $300,000. 7. But after 30 years, you would have paid "blanks" (unknown amount). 8. They have to tell you the whole story, the complete cost of credit. 9. So they're going actually what law tells you? 10. It requires the creditor to disclose a complete cost of credit. 11. My daughter went to go buy a car when she graduated college. 12. And she was smart, she didn't want me to go with her. 13. She went to do everything on her own. 14. So when she went there, she found a car with $16,000. 15. What I do want to help you come in and negotiate. 16. Well, I can do this, I'm educated up in college. 17. $16,000, here's the picture of the car, do you think? Great. 18. But then she called us back about 15 minutes later. 19. Not till she's in the back, mom, dad, you guys better come because they're trying to trick me. 20. Now, because all the paperwork shows nineteenth. 21. No, they're not trying to trick you. 22. They had to disclose the complete cost of credit. 23. After six years of paying on the car, it will be this. 24. What law says that they have to tell you that upfront? 25. Atilla since they have to disclose the complete cost of credit. 26. That's what that means...

Award-winning PDF software

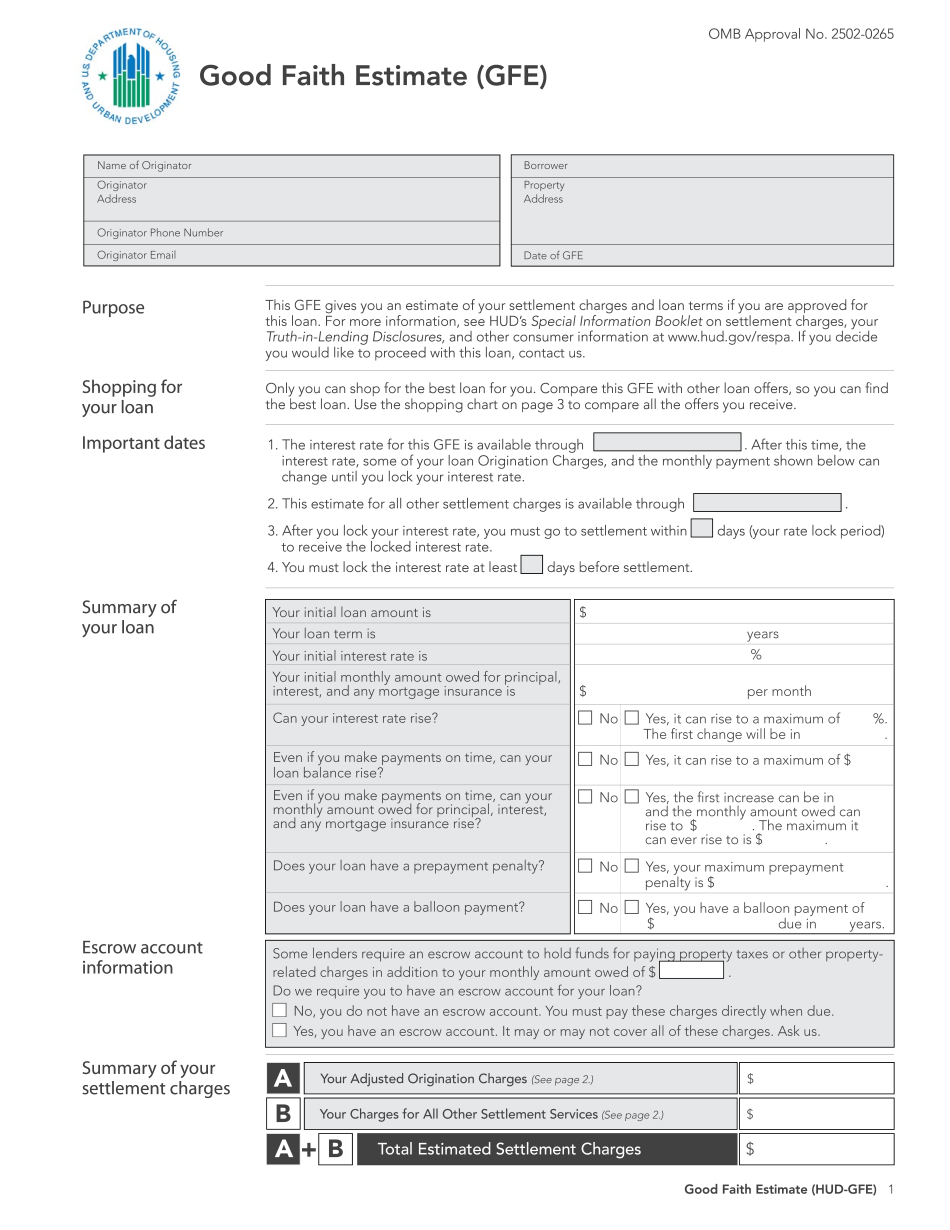

Respa Form: What You Should Know

For closed-end reverse mortgages, the HUD-1/1A and RESP are used to disclose the total origination cost of the loan on closing. The For closed-end reverse mortgage, the loan origination form is usually attached The Mortgage Settlement Procedures Act (MSA): Regulations of HUD-1/1A and RESP Regulation Z The Mortgage Settlement Procedures Act (MSA) — Federal Register, Vol. 70, No. 7067, March 8, 2010, for the purposes of section 1105 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). The Form 8300: Mortgage Settlement Procedures Act Form. (Revised December 2011) The Mortgage Settlement Procedures Act (MSA) and Regulation Z For closed-end consumer mortgage loans, the HUD-1 Form 8300 and the HUD-1/1A Regulation Z are used as a consumer's summary of settlement costs and the required title insurance information. Title insurance is a mortgage insurance coverage that covers up to 100% of the unpaid balance on the consumer's loan to make sure it is paid. The title insurance coverage is usually included in the lender's loan terms.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do HUD-Gfe, steer clear of blunders along with furnish it in a timely manner:

How to complete any HUD-Gfe Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your HUD-Gfe by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your HUD-Gfe from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Respa form