Hi everyone, I am your Tampa Bay real estate expert and realtor, Lance Moore. In this video, I want to discuss closing costs, how they work, and what you need to know about them when you're buying a home. Music Alright, let's talk a little bit about closing costs. The reason why I wanted to do this video is because we're in a really good real estate market, and I know a lot of realtors and lenders are becoming complacent. They're simply telling people to go to their website, fill out an application, and providing them with a good faith estimate that only includes the closing costs without explaining everything. First off, before I get into the closing costs, I just want to let you know that if you've been watching these videos, I'm not a big fan of big banks, especially Bank of America. In my experience as someone who has been in the lending and real estate industry for over 20 years, they often have internal problems and struggle to close deals on time. I prefer working with someone who is actively seeking business, like a mortgage banker or a broker. Now, let's discuss the difference between a bank like Bank of America or Wells Fargo, and a mortgage broker when it comes to closing costs. Banks lend their own money, so their interest rates are usually higher because they price them at retail. However, their closing costs tend to be lower compared to mortgage brokers. Mortgage brokers, on the other hand, get the pricing at wholesale, which means the interest rate may be slightly lower. However, their closing costs are higher because they have additional fees for underwriting, processing, and closing. When I mention closing costs, I am referring to the actual costs required to close a loan. I...

Award-winning PDF software

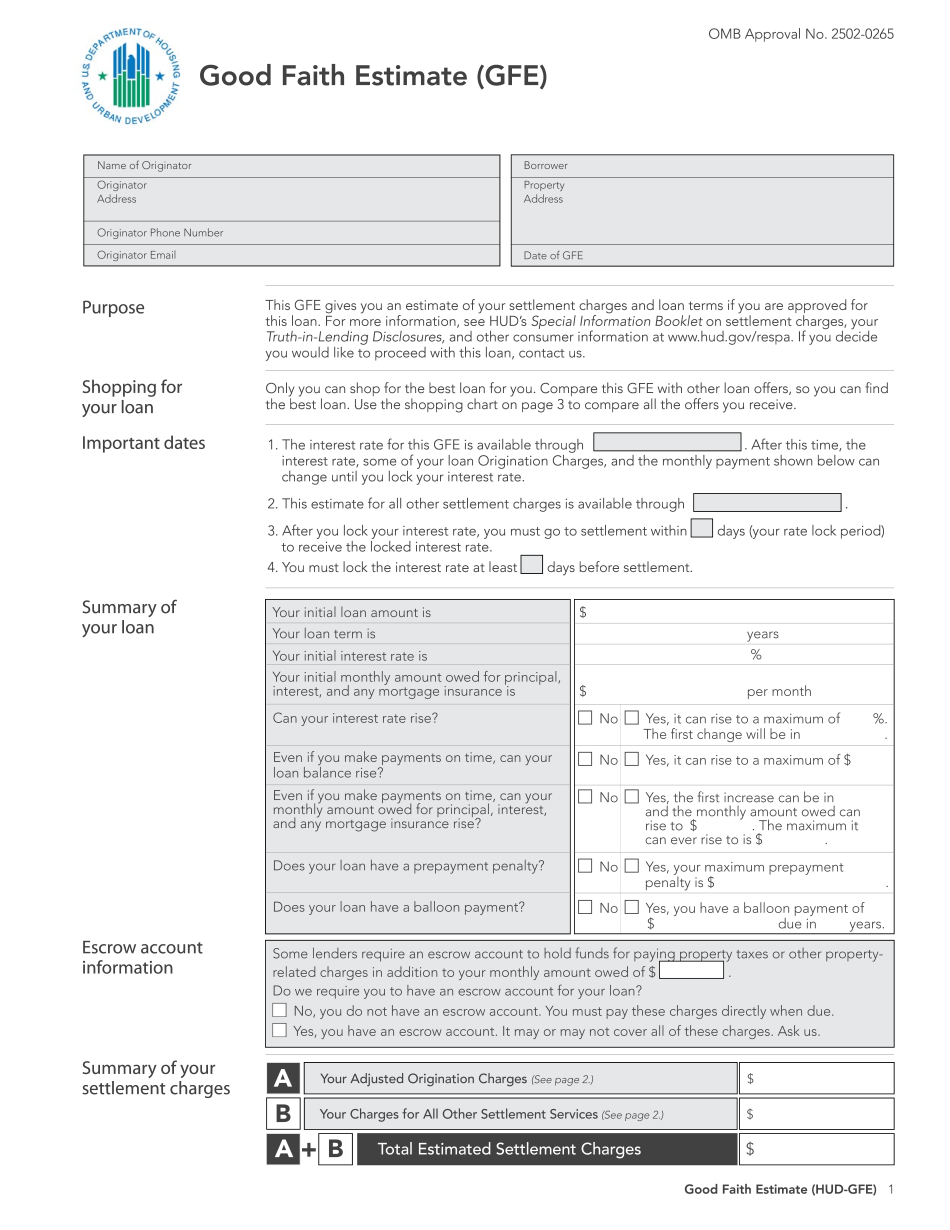

Fha closing cost calculator Form: What You Should Know

Closing Costs Calculator — Get Bankrate.com Rates Compare the closing costs, fees and rates on closing from Bankrate.com. It is your one-stop source for all-in-one home loan information — from closing costs to mortgage payment options to insurance discounts — all in one beautiful easy-to-understand calculator. Closing Cost Calculator — Mortgagee Calculate closing costs on your home mortgage in a matter of seconds with this handy calculator from Mortgagee.com. Use this calculator to estimate your closing costs from your actual closing costs. FHA Loan Calculator The mortgage application is one of the most complex components of your mortgage application, which means it will cost a lot of money to implement it correctly. But after your loan application is completed, getting it approved makes it that much quicker. FHA Loan Calculator Estimate the upfront costs on FHA mortgage loan, including down payment and closing costs. With this calculator, you will get an estimate of all the cost associated with home purchase. Mortgage Calculator — MoneySharks.com This online calculator can help you identify your mortgage, estimated rates, loan term, down payment, closing costs, and so much more. Make no mistake, once you use this mortgage calculator, you can't go back. Rent-to-Own Loan Calculator This free mortgage calculator helps you estimate upfront costs, estimated rate, estimated monthly payments based on your income and a rent. Enter your income, mortgage amount, down payment, and closing costs to get all the information needed about your mortgage application. Mortgage Calculator — Mortgagee If you are making mortgage payments you will need to pay something to the landlord for letting you use their property to make payments on your mortgage. However, you don't know what that will be. This calculator helps you guess whether you own and lease. Mortgage Closing Costs — SimpleMoneyLines There are two basic types of lending: Fannie Mn's and Freddie Mac, and you pay different costs based on whether you get a Freddie Mac, or Fannie Mn's, loan. FHA Loans — Get the Best Rates FHA Loan Calculator Estimate the closing costs on your FHA home mortgage, including fees and closing costs. Get the exact figures as they will be different depending on which type of loan you choose.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do HUD-Gfe, steer clear of blunders along with furnish it in a timely manner:

How to complete any HUD-Gfe Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your HUD-Gfe by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your HUD-Gfe from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Fha closing cost calculator