October 3rd, 2015 marks the day when the mandatory trade begins, bringing significant changes to the real estate closing process. It is important for buyers, also known as borrowers, falling within trade guidelines to understand what to expect when purchasing a home. All borrowers falling under trade guidelines will receive the Loan Estimate (LE). This form provides an estimation of the fees involved in the closing process, and lenders are required to provide accurate fees within three days of loan application. In addition to the LE, borrowers will also receive the Closing Disclosure (CD) at least three business days before the closing. It is crucial for lenders to deliver the CD within this timeframe; otherwise, there will be a delay in the closing process. Before the implementation of trade, buyers would meet with a lender and undergo a loan application process. The lender would gather information on the borrower's income, and sometimes even ask unrelated questions, such as salary expectations if they had their dream job or asking them to blow into a breathalyzer. While not all lenders engaged in questionable practices, the 2008 mortgage crisis prompted the signing of the Dodd-Frank Act by the President on July 21st, 2010, which led to the establishment of the Consumer Financial Protection Bureau (CFPB) on the same date in 2011. CFPB is an independent agency responsible for consumer protection within the financial sector. It enforces laws and regulations in the mortgage industry and allows consumers to voice their complaints if they feel mistreated. Violators of these laws can face fines of up to 1 million dollars per day per violation. Now let's dive into the closing process for borrowers falling under trade guidelines. The process mainly affects mortgage lenders, with various forms that require signatures. At closing, buyers and sellers used to meet at the attorney's office...

Award-winning PDF software

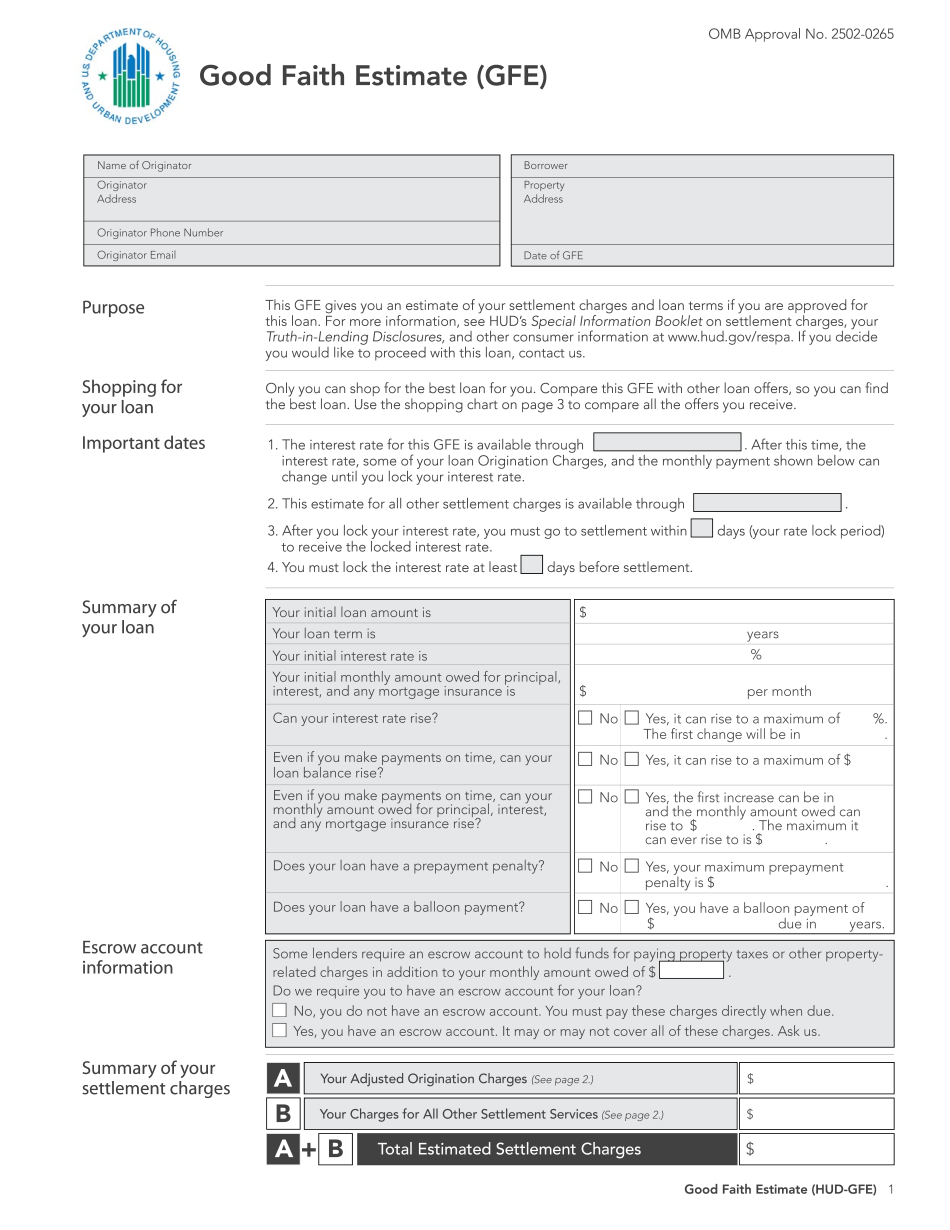

Respa disclosures Form: What You Should Know

Faces-Off for DSP (M-2.1) ». This is a summary of the DSP program for individuals using Income-Based Repayment. The final form is expected to be released in 2013. Model DSP Summary (M-2.2) ». Model DSP Summary (M-2.3) ». This is an overview of the income-based Repayment program and its structure. Model Income-Based Repayment Overview for Borrowers An overview of the income-based repayment program and the program structure. Model Income-Based Repayment Overview ». The forms were used with the help of a software project. Testimony of the Test Pods Testimony of the Test Pods was prepared for the Public Service Review on the use of the DISC model of disclosure forms. Testimony of the Test Pods — Public Service Review Hearing Transcript. Testimony of the Test Pods—Public Service Review Hearing Transcript. — Transcript. Testimony of the Test Pods — Public Service Review Hearing Transcript. — Translation. Testimony of the Test Pods—Public Service Review Hearing Transcript. — Language PDF. Statement of Testimony on Testimony in Public Hearing Testimony in Public Hearing — Transcript. Testimony of the Test Pods. — Transcript. Testimony of the Test Pods. — Transcript. Testimony of the Test Pods.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do HUD-Gfe, steer clear of blunders along with furnish it in a timely manner:

How to complete any HUD-Gfe Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your HUD-Gfe by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your HUD-Gfe from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Respa disclosures