Hey everybody, what is a good faith? Ehey Rob Castro coming to hear from la Orange County area. So cal and today talking about what is a good faith? Eget this question all the time. Everybody's heard of a good faith, ebut a lot of buyers borrowers are kind of unclear on what is it exactly. So when you go to the lender to get pre-approved pre-qualified, you fill out a loan application. They're required to give you a good faith, ewithin three days from you filling out your application. So this is an ethat's going to come from your loan officer, mortgage banker, mortgage broker, and what, what is it? So it outlines all the costs of your loan, all the costs of your transaction, basically. So it's going to outline closing costs, lender fees, escrow, and title fees, interest rates, underwriter processor fee, all of those kinds of things right in black and white for you up front which is awesome. It's good information for you to know and, most importantly, it outlines what your payment's going to be, taxes, insurance, principal interest, all that stuff. So you know upfront. So this is a good thing to have, especially when you're shopping around for a loan. If you're shopping different banks, different lenders, you get one from each of them and you can clearly see what every single costs and fees going to be, you can compare, you can see if somebody's offering you a higher rate than somebody else, higher closing costs, etc. This is also good to keep when you know you get one in the beginning and when you first get pre-qualified and who knows it might take you a little bit of time to find a place so you might be looking for a...

Award-winning PDF software

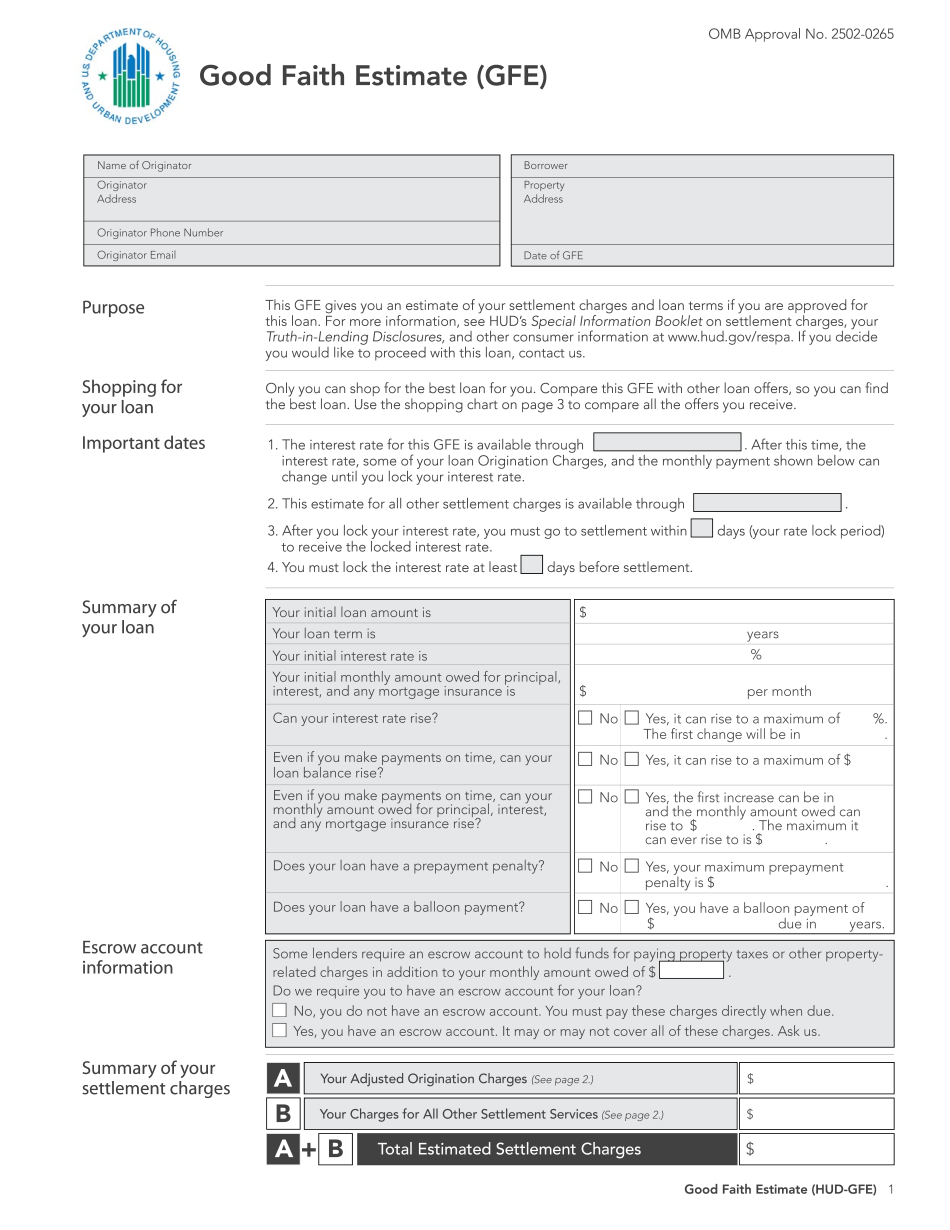

Good faith evs actual closing costs Form: What You Should Know

HUD-1 Form For Loan Recipients With A Lender That Offers A Loan-to-Value Reduction. HUD-1 Form (for borrowers that are offered a loan-to-value reduction only) HHS-10-8 HUD-1 Form The Housing and Urban Development (HUD) has issued an administrative rule (44 FR 87955) that clarifies the requirements for the HUD-1 Form and the HUD-1 (or HUD-2) Form that is used for processing of loans with a GFE which includes: a. HUD-1 Form. The HUD-1 form is used to provide borrowers with a HUD-1 form, which includes all information required for a Loan Estimate or GFE including, but not limited to, information regarding expected loan payments, borrower debt, property appraisal, property ownership history, taxes, insurance and a loan estimate that is used by lenders for loan approval. b. HUD-2 Form. The HUD-2 form is used to provide borrowers with a HUD-2 form, which includes all information required for a Loan Estimate or GFE including, but not limited to, information regarding expected loan payments, loan term, expected principal and estimated interest rates. a. General Disclosure Statement — the HUD-2 form (1) The Mortgagee (Lender) of Record in the case of a loan that is subject to the terms of a HUD-1 Form shall, when requesting, providing or using the HUD-2 Form, include a statement in the Mortgagee's application for loan approval that is substantially similar to the following: (i) An initial description of the property described in the HUD-1 form. (2) The Mortgagee cannot use the HUD-2 form to identify the borrower unless the borrower's name, address and telephone number are included in the HUD-1 form. (3) Loan Estimate. An estimate of the payment and the amount that the Mortgagee believes the borrower will pay the Loan in repayment of the principal balance of the loan when fully paid.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do HUD-Gfe, steer clear of blunders along with furnish it in a timely manner:

How to complete any HUD-Gfe Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your HUD-Gfe by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your HUD-Gfe from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Good faith evs actual closing costs