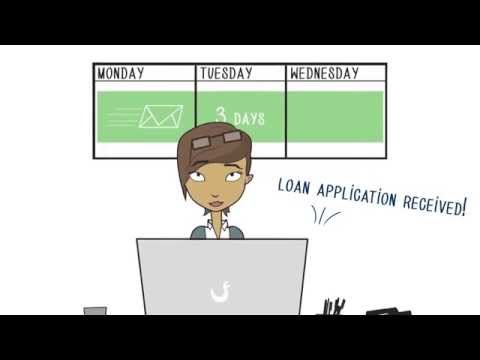

New forms and new rules from the Consumer Financial Protection Bureau go into effect beginning August 1st, 2015. Know before you close, the new loan eform replaces the early Tila disclosure and a good faith eit lists all the potential costs for the consumer's loan, such as title insurance percentage rates, closing costs, and the estimated monthly loan payment. Creditors are responsible for calculating the best estimates possible for these services, which will be checked against the actual costs listed in the closing disclosure form when the loan is consummated. Unlike the former Good Faith Ecreditors, creditors can no longer revise and readjust charges if they go up or down prior to closing. After all, resetting the eevery time a circumstance changes weakens the purpose of the eonce. Once a consumer's application is received, the creditor has three days to deliver the loan eand should include a list of providers for services the consumer can shop around for. Forms, dates, rules, and laws can seem like a lot to take in. The good news is that we've done our homework and we're here to guide you through. To learn more about how the CFPB changes impact you, contact a local representative.

Award-winning PDF software

Good faith ereplaced by Form: What You Should Know

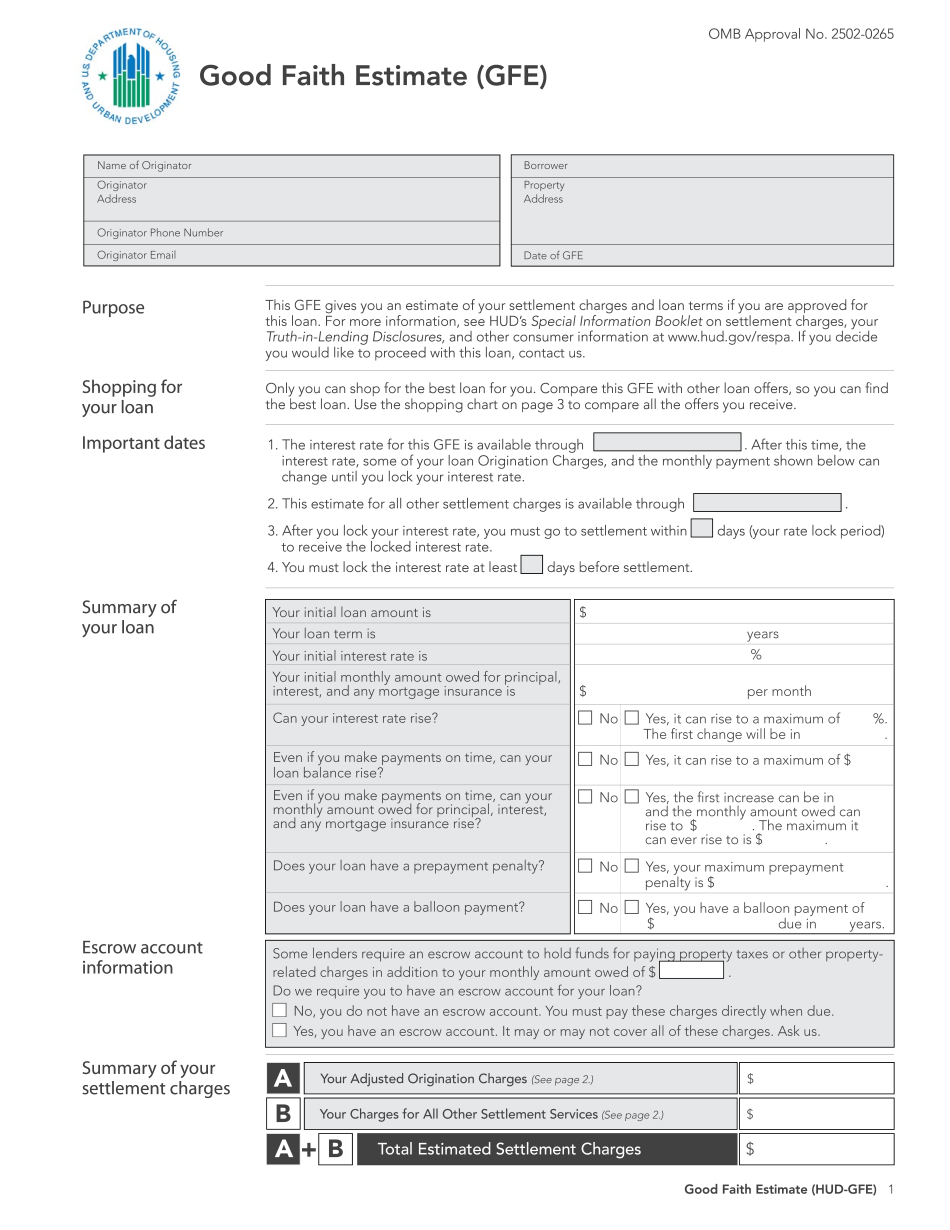

HUD-1 & HUD-1A Uniform Settlement Statement Form HUD-1, HUD-1A. The Truth-In-Lending (TIL) & the Good Faith Estimate. The Truth In Lending Form has gone through a major redesign to improve its functionality and to make it easier and faster to use Good Faith Estimate FAQ 13.04.10.00 — HUD-1 & HUD-1A Uniform Settlement Statement Form Good faith estimates are required by the Federal Housing Administration [FHA] and are part of the mortgage documents required to be provided to prospective buyers. The following is a copy HUD-1, HUD-1A and TIL — What is a Good Faith Estimate? Aug 4, 2024 — A Good Faith Estimate, also called a GFE, is a form that a lender must give you when you apply for a reverse mortgage. The final changes to HUD-1, HUD-1A, Disclosures for New Uninsured/Self-Pay Individuals The disclosures and the information in the disclosure are the same as before the new HUD-1 forms and information about how the credit score application process may vary depending on the applicant's credit report and a summary table has been designed to help you understand the terms of your application. Loan Estimate FAQ 13.24.2021 Final — HUD-1 & HUD-1A Uniform Settlement Statement Form Disclosure — HUD-1, HUD-1A and TIL — What is the Good Faith Estimate? How the Good Faith Estimate Works A borrower may use a Good Faith Estimate when applying for a reverse mortgage. It is important for the prospective buyer to review the information in the GFE in order to understand the lender's underwriting practices and to make sure that the information provided in their GFE is true and complete. In addition, lenders may seek additional information from the borrower and may require documentation from the borrower as part of their process. A borrower who believes they have been misinformed about any financial product or transaction may choose to provide additional information to clarify or otherwise correct this information.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do HUD-Gfe, steer clear of blunders along with furnish it in a timely manner:

How to complete any HUD-Gfe Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your HUD-Gfe by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your HUD-Gfe from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Good faith ereplaced by