Music. Hi everyone, this is your Tampa Bay realtor, Lance Moore. In this video, I want to go over Ego Home Mortgage closing costs. I generally don't like to do this, but if you don't know, Ego Home Mortgages is owned by O&R. And you know, one of the first states, the reason why I'm doing this is because I have a gentleman who is buying a new home, and he was very confused on all these costs because unfortunately, a lot of the lenders for these mortgage companies, what the builders are very complacent. They're not taking the time to go over everything with consumers. Consumers and my clients are always calling me on this, asking me questions because they know I know a lot about mortgages. I used to be in mortgage banking, so I don't like doing this because I know, for example, if you're in California, if you're in Texas, there could be completely different costs. Things are completely different. I'm doing this in Tampa, Florida, and these are the costs, and the costs are what the costs are today, and there are typical costs in our area. So really, I want you to take this with a grain of salt. And I've gone over this before with people. There are basically three different types of lenders out there. There are the banks. I'm not a big fan of the banks, as most people know because if they have a round hole and you're a square peg, you don't fit very well. They just tell you you don't qualify. You know, they only have their money to lend, and they're basically just fault rates are not really a master of anything. When you get into companies like Eagle Home Mortgage, they're a banker. They most likely are lending...

Award-winning PDF software

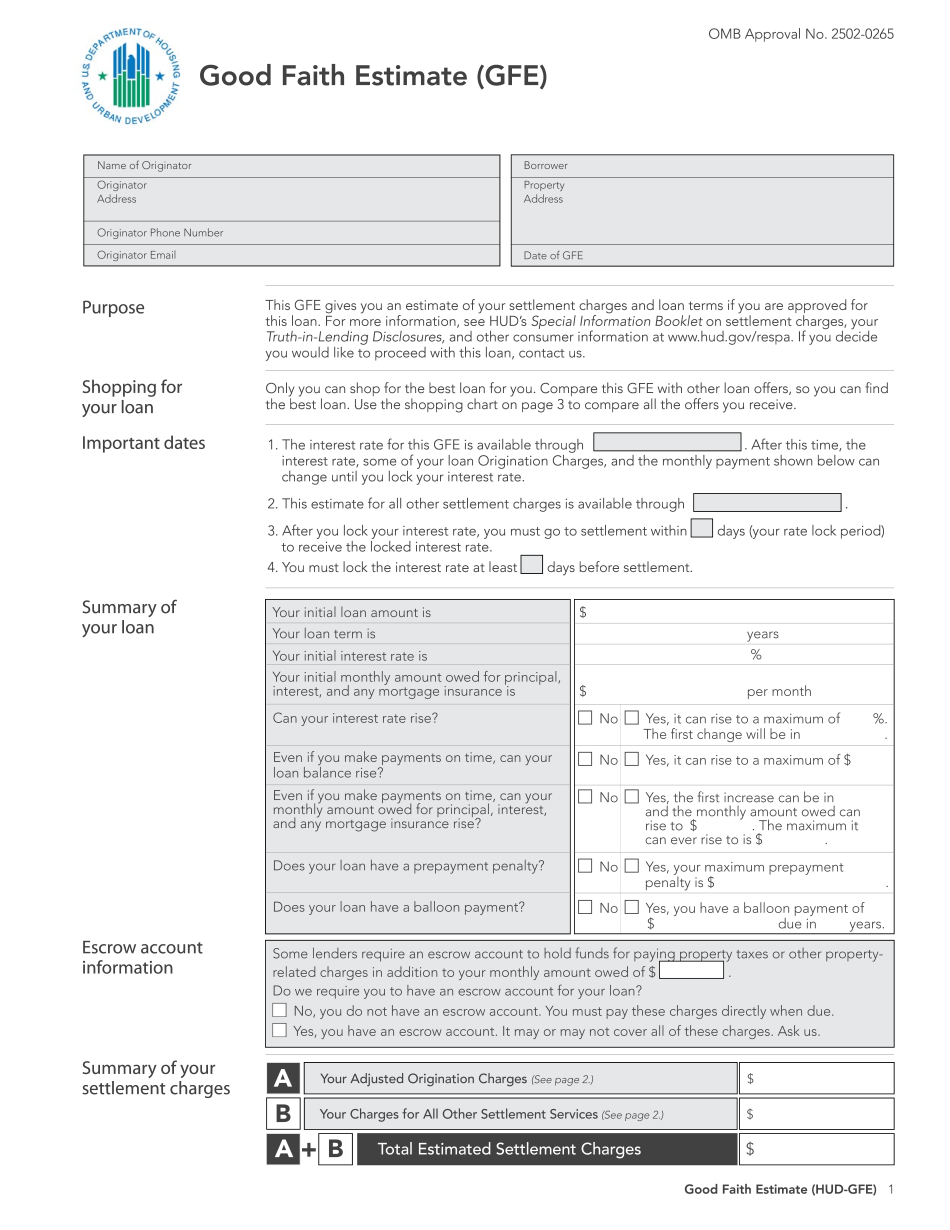

Good faith evs loan estimate Form: What You Should Know

It was used by HUD for determining if applicants were approved for the loan. It was then placed in the customer's file, which is kept by the lender. Under a new loan regulation, the Good Faith Estimate has been replaced with the loan estimate. In October 2010, the new rules became effective. The borrower is responsible for calculating a loan estimate, in accordance with the new Home Equity Loan Disclosure Act (HELD). This means we now have the responsibility for knowing how to accurately calculate our own estimate. What is a good faith estimate? There are several factors that should be considered when calculating the loan estimate. There are three questions to ask about the estimated price: 1) Is the estimate based on current market conditions or on other information regarding the home purchase? 2) What is your plan for the loan based on the information on the GFE. 3) Are you eligible for the loan if you make the loan under these terms and conditions? How To Calculate your Good Faith Estimate. 1) First, you need to establish the estimated size of your loan and take into account current market conditions and information on the GFE. The size of a traditional 30-year loan (a 30-year fixed rate home mortgage has a variable rate based on changes in the Treasury Note rate over the life of the loan. This means any loan that was sold in the prior year (like a 1-year fixed note) or any loan that was sold at a different price than the fixed rate will change the annual interest rate after the GFE has been calculated. The size of a typical 30-year loan is dependent on the interest rate on the Mortgage Note and a handful of other factors (including your mortgage's down payment and any interest paid on your other loans). The GFE does not reflect this specific market information. To calculate the estimated length of your loan, you need to take your current equity in the home, and divide it by the size of your loan. This equals your estimated equity length (even = the number of years left to pay off the loan). To help you remember how to calculate this number, imagine your mortgage balance is 50,000, and you have 7000 to pay off the debt the first year. If you have no other expenses (like a down payment, closing costs and property taxes), you can rest assured that you have over 7000 remaining to pay the loan off after the GFE is calculated.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do HUD-Gfe, steer clear of blunders along with furnish it in a timely manner:

How to complete any HUD-Gfe Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your HUD-Gfe by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your HUD-Gfe from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Good faith evs loan estimate