Filling in your self-assessment involves completing an online or paper tax return. This tells HM Revenue & Customs about your income and any capital gains or enables you to claim tax allowances or reliefs. There are deadlines for sending in your tax return and penalty charges if it's later, so make sure you get it in on time. Not everyone needs to complete a tax return. However, if you're not already paying tax by pay-as-you-earn or a higher rate taxpayer or have complicated tax affairs, you will need to complete a self-assessment return. To be clear, if you're self-employed, earn more than £100,000 a year, or have complicated tax affairs (for example, multiple income streams), then you will need to complete a tax return. Company directors and faith ministers are also required to complete one, irrespective of their financial affairs. HMRC also sends some out randomly during the tax year, which runs from the 6th of April one year to the 5th of April the following year. The key dates for sending in your tax return are the 31st of October for paper returns and the 31st of January for returns made online. If your affairs are reasonably straightforward, you may be sent the short return called an SI 200, which is only four pages long. The accompanying notes will help you fill it out. This cannot be submitted online though, so if you prefer to file online, you will have to complete the full return. If you're doing a paper return, first check that you've got the right pages. Missing pages can be downloaded from the HMRC website. You should have two core forms, the SI 100 and the SI 101, as well as relevant supplementary pages (for example, for employment income or income from property). Next, you need...

Award-winning PDF software

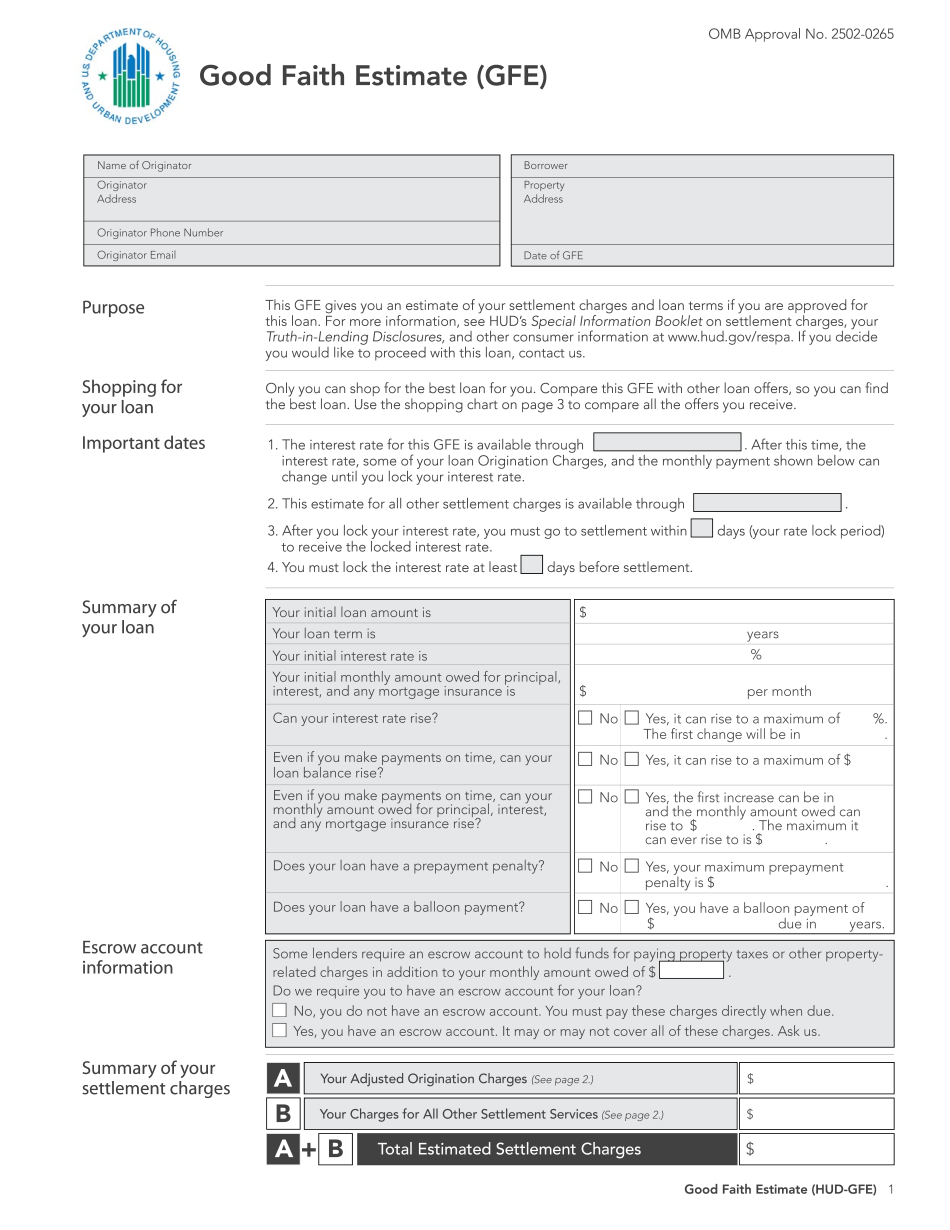

HUD-Gfe Form: What You Should Know

The new GFE can be printed at home or downloaded at that link. Good Faith Estimate (GFE) — Section 5 of Responsible Lending Reform This form is required and used when dealing with the Section 5 of REP and this particular loan. Good Faith Estimate (GFE) is a standard form for an REP loan. GFE for Section 5 of REP (Good Faith Estimate) — Department of Housing and Urban Development (HUD) Archives This is information on the Good Faith Estimate (GFE) that is posted under the section 5 of RESP in the Department of Housing, Urban Development, and Related Agencies Home Mortgage Disclosure Act and its regulations under the FLB (HUD). This is information on this form that is posted in May 2005 GFE For Good Faith Estimate (GFE) — HUD Archives This GFE is required when processing a loan on a nonconsidered basis under Section 5 of RESP. This is information on the GFE (good faith estimate) that is published for the Department of Housing and Urban Development (HUD) and REP Loan Applications The following is information on the GFE that has been published for RESP during January 2024 and later. This is information on this form that the Federal Home Loan Bank of America (FLB) and/or other regulated entities should use to determine the GFE on the RESP. If you are considering a nonconsidered loan on a REP, there must be an approved GFE form and payment schedule for the REP Loan. For nonconsidered loans, you must have a GFE that 1) lists loan payments for principal, interest, escrow, and taxes; and 2) accounts for all fees, charge offs, and other charges. GFE for Good Faith Estimate (GFE) — HUD Archives This GFE (good faith estimate) is the form you will need when processing an REP and a good faith estimate for the REP loan.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do HUD-Gfe, steer clear of blunders along with furnish it in a timely manner:

How to complete any HUD-Gfe Online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your HUD-Gfe by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your HUD-Gfe from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing HUD-Gfe